Introduction

The 2026 Spring Statement (3 March) outlined the Government’s fiscal strategy in response to ongoing economic challenges, including those in the Middle East, with a laser-sharp focus on defence spending, as well as education, early years education and welfare reforms.

Against a backdrop of reduced short-term growth, increasing unemployment, and inflation falling quicker than previously forecast, the Chancellor of the Exchequer, Rachel Reeves, announced that her fiscal headroom should increase by around £2 billion, thereby making another tax rise in the 2026 Autumn Budget less likely.

As expected, The Chancellor did not make any policy overhauls, maintaining her steadfast approach to only holding one major fiscal event per year.

Therefore, notable changes to the Vehicle Excise Duty Expensive Car Supplement for zero-emission cars, as well as Capital Allowances will still come to into effect from April 2026, together with the introduction of a Benefit in Kind tax easement for plug-in hybrid electric vehicles, which is already in place.

Plug-in van grants remain unchanged, and the temporary reduction in Fuel Duty will also continue through to end of August 2026 and will rise in line with inflation from April 2027.

We have again summarised the current policies and impending changes relating to the vehicle leasing industry and how these could impact you.

Vehicle Excise Duty

Expensive Car Supplement

The VED Expensive Car Supplement will be uprated in line with inflation from 1 April 2026, rising from £425 to £440.

In 2025/26, all cars, including zero-emission cars, registered on or after 1 April 2025, with a list price of £40,000 or more are subject to the expensive car supplement, which applies from year two, for five years following the first year’s registration.

For zero-emission cars, the VED Expensive Car Supplement threshold will rise to £50,000 from 1 April 2026. It will apply retrospectively for zero-emission cars registered from 1 April 2025, unless the car is sold before April 2026 when the £40,000 threshold will apply to the new owner for one-year.

Electric Vehicle Excise Duty

An important announcement made during the 2025 Autumn Budget, potentially setting out a roadmap for the long-term funding of Britain’s highways, was the proposed launch of electric Vehicle Excise Duty, or eVED.

Subject to the Government’s consultation, which will run until 18 March 2026, the following pence per mile (ppm) charges will be introduced from 1 April 2028:

· Zero-emission cars - 3ppm;

· Plug-in hybrid electric cars - 1.5ppm

These rates will rise in line with inflation each year thereafter.

Based on the average EV owner driving 8,000 miles per year, they will pay an additional £240 per year in 2028/29.

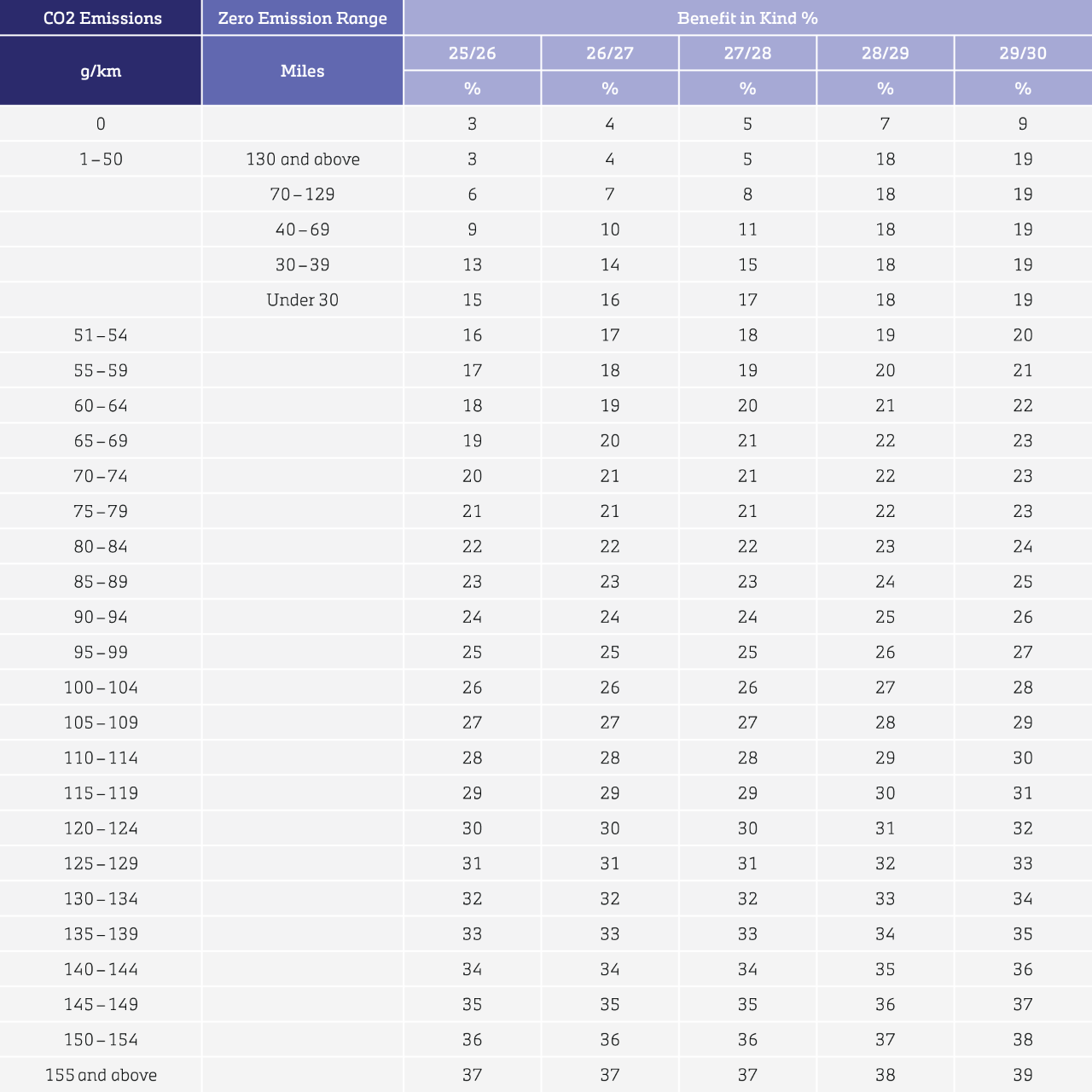

Company Car Tax

From 6 April 2026, the BiK tax rates for cars with:

· zero-emissions will rise to 4%; thereafter, the rates will rise by 1% in 2027/28, and 2% in each of 2028/29 and 2029/30 to reach 9%;

· CO2 emissions between 1-50g/km, BiK tax rates will rise by 1% per year until 2027/28, before jumping to 18% in 2028/29 and 19% in 2029/30;

· CO2 emissions between 50-74g/km, the rates will rise by 1% per year to 2027/28, subject to a maximum of 21%, then rise again by 1% per year in each of 2028/29 and 2029/30;

· CO2 emissions from 75g/km, BIK tax rates will be frozen for two years before rising by 1% per year in each of 2028/29 and 2029/30.

The maximum rate of BiK tax, which has been capped at 37% for many years, will increase by 1% per year for two years starting in 2028/29, reaching a new cap of 39% in 2029/30.

For non-RDE2 (Real Driving Emissions Step 2) diesels, a BiK tax supplement of 4% will continue to apply, subject to the maximum rate mentioned above.

Example:

Consider a fully electric car with a P11D value of £48,495 and CO2 emissions of 0g/km; its BiK tax band for 2026/27 is 4%.

£48,495 x 4% gives a taxable value of £1,940 and yearly BiK tax charge of £388 (£32/month) for a 20% taxpayer, £776 a year (£67/month) at 40%, and £873 a year (£73/month) for a 45% taxpayer.

Footnotes on BiK chart:

1. A car propelled solely by diesel which does not meet the Real Driving Equivalent (RDE) Step 2 standard will be subject to a first-year rate equivalent to the band above its actual emissions, up to the maximum of £5,490.

2. There is no alternative fuel discount available for any car from April 2025, regardless of when it was first registered.

3. All cars, excluding those with zero emissions registered before 1 April 2025, with a list price greater than £40,000 when new will be subject to an annual £425 expensive car supplement on top of the standard rate for 5 years.

4. A car propelled solely by diesel which does not meet the Real Driving Equivalent (RDE) Step 2 standard will be subject to a first-year rate equivalent to the band above its actual emissions, up to the maximum of £5,690.

5. All cars with emissions greater than 0 g/km and a list price greater than £40,000 when new will be subject to an annual £440 expensive car supplement on top of the standard rate for 5 years. All zero-emission cars registered from 1 April 2025 with a list price greater than £50,000 when new will be subject to the annual £440 expensive car supplement, but zero-emission cars registered before 1 April 2025 are exempt.

PHEVs – Re-homologation

Due to the re-homologation of plug-in hybrid electric vehicles (PHEVs) under the Euro 6e-bis standards, the CO2 emissions of many PHEVs will increase. It will result in a significant increase in BiK tax for up to 150,000 company car drivers.

To mitigate the impact of these changes, a temporary BiK tax easement will apply, retrospectively from 1 January 2025 where:

· a car was first registered on or after 1 January 2025;

· a car’s CO2 emissions figure is 51 or more;

· a car was not registered under the Euro 6d-ISC-FCM or Euro 6e standards; and

· a car’s electric range figure is one or more.

For a PHEV company car made available on or before 5 April 2028, the easement will apply subject to transitional arrangements until 5 April 2031.

This change will also reduce the Class 1A National Insurance Contributions (NIC) payable by employers, but it does not apply for VED or to the lease rental restriction.

For PHEVs made available up to 5 April 2028, the BiK tax easement will apply until 5 April 2031, subject to transitional arrangements coming into effect from April 2028.

Example:

Consider a plug-in hybrid car, with a P11D value of £49,055, official CO2 emissions of 20g/km tested under Euro 6, and a zero-emission range of 62 miles; it will have a BiK tax percentage of 10% in 2026/27.

Following re-homologation under Euro 6e-bis the official CO2 emissions have risen to 60g/km, increasing the BiK tax rate to 19%, but the PHEV easement means that for BiK tax purposes its emissions would be deemed to be 1g/km.

The easement would therefore return the BiK tax percentage to 10%, meaning the BiK tax and Class 1A NIC would be calculated as follows:

BiK tax - £49,055 x 10% gives a taxable value of £4,905, with a yearly BiK tax charge of £981 (£82/month) for a 20% taxpayer, £1,962 a year (£164/month) at 40%, and £2,207 a year (£184/month) for a 45% taxpayer.

The Class 1A NIC charge would be £736 (£49,055 x 10% x 15%).

Capital Allowances

Capital Allowances provide tax relief on the costs of capital assets, such as cars and vans, in place of commercial depreciation on which tax relief is not available. Capital Allowances are claimed either over several years via writing down allowances (WDAs), or all at once via a first-year allowance (FYAs), with excess relief being repaid over many years after the sale of the vehicle by the business.

The 100% first-year allowance (FYA) for zero-emission cars, and electric vehicle charge-points, will be extended by one-year to April 2027.

The main rate of WDAs has been set at 18% per year since 2012. This rate will be reduced from to 14% per year, effective from April 2026, meaning tax relief will be restricted for cars with CO2 emissions between 1 and 50g/km.

For cars with emissions exceeding 50g/km, i.e. those qualifying for the special rate of WDAs, the annual rate will remain at 6%.

Lease Rental Restriction

Lease rentals on company cars can be offset against tax, with the threshold set at 50g/km of CO2. New cars with CO2 emissions of 50g/km or less are eligible for 100% of the lease rentals to be offset, while only 85% is claimable for those with CO2 emissions of 51g/km or more.

There are no proposed changes to the threshold or the percentage that can be deducted for higher emitting cars.

Grants

Electric Car Grants

It was announced in the 2025 Autumn Budget that the electric car grant, launched in July 2025, will be supported by an additional £1.3 billion of funding, enabling its availability to be extended until 31 March 2030.

The level of the grant available on the purchase of a qualifying zero emission car is subject to the manufacturer’s commitment to a verified Science Based Target and which have embodied carbon scores below a certain threshold in vehicle assembly and battery cell production locations.

Level of grant available

Band 1 – Cars with lowest carbon emission scores £3,750

Band 2 – Cars with higher carbon emission scores £1,500

Cars made by manufacturers who have not a set science-based target are not eligible.

Eight cars currently qualify for the Band 1 maximum grant of £3,750; these are the new Nissan Leaf, Citroën ë-C5 Aircross Long Range, Ford E-Tourneo Courier, Ford Puma Gen-E, MINI Countryman, Renault 4, Renault 5, and Renault Alpine 290.

For a list of cars that qualify for the Band 2 grant of £1,500, visit Gov.UK.

EV Chargepoint Grant

The availability of an EV Chargepoint Grant has recently been extended until 31 March 2027. The grant provides up to 75% of the installation cost of a charge point, up to a maximum of £500 and is available to homeowners who live in flats, or individuals who live in rented accommodation.

The grant available may vary across the regions and nations of the UK; for example, until 31 March 2027 an EV Chargepoint Grant is available to those with access to on-street parking from certain local authorities in England.

For more information on grants visit Gov.UK.

The extension of the chargepoint grants follows the announcement made during the 2025 Autumn Budget regarding an array of funding and other measures to support chargepoint rollout, as follows:

· £100 million for local authorities and public bodies to support the training and deployment of specialist staff to accelerate the rollout of public chargepoints;

· £100 million, in addition to £400 million already announced, to invest in EV charging infrastructure, including the installation of home and workplace chargepoints; it aims to accelerate the rollout of cross-pavement charging solutions, to make EV charging easier, cheaper and more accessible for households without driveways; and a 10-year 100% business rates relief programme for eligible EV chargepoints and EV-only forecourts

Business Mileage Reimbursement

Company Cars

With effect from 1 March 2026, the Advisory Electricity Rate (AER) for public charging was increased to 15p per mile.

Advisory Electricity Rates* Electricity

Home charger 7p

Public charger 15p

*The AER applies to all cars powered solely by electricity and does not apply to range extended cars or plug-in hybrids, for which the AFRs should be used.

The petrol and diesel Advisory Fuel Rates (AFRs) have not changed compared to the previous quarter.

Advisory Fuel Rates Petrol LPG

Engine size

1400cc or less 12p 10p

1401cc to 2000cc 14p 12p

Over 2000cc 22p 19p

Advisory Fuel Rates Diesel

Engine size

1600cc or less 12p

1601cc to 2000cc 13p

Over 2000cc 18p

Hybrid cars are treated as either petrol or diesel cars for these purposes.

Private Cars

HMRC Approved Mileage Allowance Payments (AMAPs), are income tax and NIC-free amounts claimable by a driver using their own car for business mileage; these have been frozen for many years and are shown below for 2026/27.

· Up to 10,000 miles – 45p per mile

· Over 10,000 miles – 25p per mile

Employees using cars or vans on business journeys while carrying fellow employees as passengers can be paid an additional 5p per mile free of income tax and NIC.

For NIC purposes, the qualifying amount (the amount that can be paid without the need to apply NIC), is 45p per mile, regardless of the business mileage undertaken. Therefore, the 10,000-mile threshold does not apply for the purposes of NIC.

Fuel Duty

The longstanding freeze of fuel duty will end in 2027 when it will again be uprated in line with inflation, with the temporary cut introduced in 2022 being reversed gradually, as outlined below:

· 1p on 1 September 2026;

· 2p on 1 December 2026; and

· 2p on 1 March 2027 (returning rates to pre-March 2022 levels).

Commercial Vehicles

Benefit-in-kind (BiK) tax

The van benefit charge (VBC) for those driving a company van for private use is set to increase in line with inflation to £4,170 in 2026/27.

The VBC for private fuel use will rise to £798.

The monthly tax payable in 2026/27 is shown below:

· Monthly Bik tax (excl. fuel) - £69.50/£139.00

· Monthly BiK tax (incl. fuel) - £82.80/£165.60

Figures shown for 20%/40% taxpayers.

Class 1A NIC

Class 1A NICs are calculated based on the Van Benefit Charge. The amounts due are calculated by multiplying the VBC by 15%, with the charges for 2026/27 shown below.

· Annual Class 1A NIC (excl. fuel) - £625.50

· Annual Class 1A NIC (incl. fuel) - £745.20

Capital Allowances

Purchased vans (other than those bought for leasing) qualify for full expensing, which enables companies to deduct 100% of the purchase price from their profits before tax, albeit tax is payable on the disposal proceeds on sale.

However, full expensing is not available to companies that buy vans to lease, or unincorporated businesses. To partially compensate these businesses, and to power investment, a new FYA of 40% was introduced for vans purchased on or after 1 January 2026. After the year of purchase these vans will qualify for WDAs at 14% per annum.

London ULEZ and Congestion Charge

From 25 December 2025, electric vehicles (EVs) were subject to the Congestion Charge, with the charge increasing on 2 January 2026 from £15 to £18 per day, if paid on the day, and from £17.50 to £21 if paid within three days.

Congestion Charge Residents' Discount holders will still receive a 90% discount and pay the daily charge of £1.80. Existing discount holders will keep the 90% discount for all vehicle types, including new and replacement vehicles, whether they are electric vehicles or not. For new applicants, the discount will only apply to electric vehicles.

EVs registered for Transport for London’s (TfL) Auto Pay will receive a 25% discount on the Congestion Charge, with electric vans, HGVs and quadricycles receiving a 50% discount, if registered for Auto Pay.

As the eligible vehicle numbers are expected to grow over time the discount level will reduce from 4 March 2030 to 12.5% for electric cars and 25% for electric vans, HGVs and quadricycles, provided they are registered on Auto Pay.